The Sacramento region’s spring housing data, newly released by Redfin for the three months ending in April, shows a market splitting in two directions at once. Granite Bay’s median sale price surged 20.9% from a year earlier to roughly $1.46 million, even as five of the eight cities tracked saw prices fall year over year. Sales activity, meanwhile, picked up in most of the region — six of eight cities recorded more closings than they did a year ago — suggesting buyers are re-engaging despite uneven pricing signals.

The backdrop is a national mortgage market that has eased modestly. Freddie Mac data published by the Federal Reserve shows the 30-year fixed rate averaged 6.33% in April 2026, down from 6.72% a year earlier but up from 6.18% in March. The S&P/Case-Shiller U.S. National Home Price Index was essentially flat year over year in its latest reading, underscoring that the price strength seen in pockets of the Sacramento suburbs is not a national pattern.

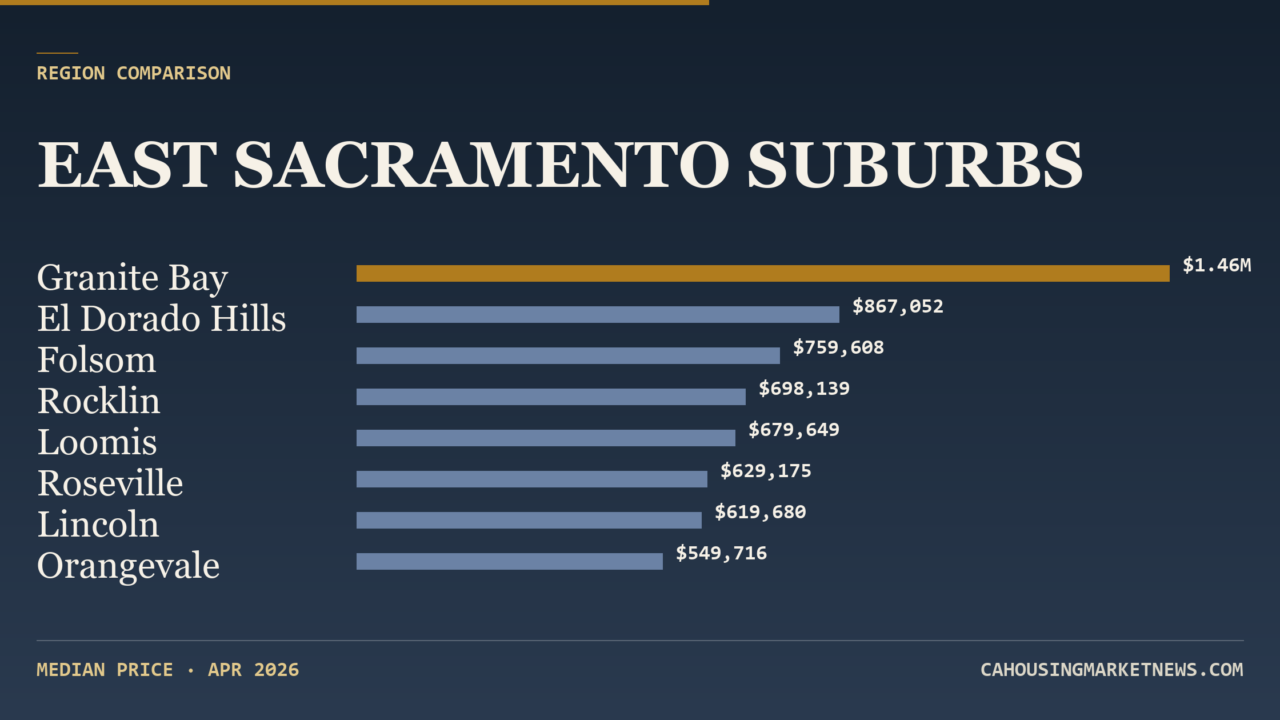

Prices: Granite Bay surges, Loomis tumbles

Granite Bay posted the largest year-over-year price gain in the region, with its median climbing 20.9% from $1,207,000 to $1,459,246, according to Redfin. It is also the most expensive city in the comparison by a wide margin — more than $590,000 above the next-highest market, El Dorado Hills. Granite Bay’s gain came alongside a 9.5% drop in homes sold (from 63 to 57) and a median days-on-market that rose from 20 to 36, suggesting the price figure reflects a thinner, higher-end mix of transactions rather than broad-based bidding pressure. With only 57 closings, small sample sizes can produce outsized percentage swings.

Rocklin was the only other city to post a clear price gain, with its median rising 4.2% from $670,000 to $698,139. Folsom was essentially flat, up 0.5% to $759,608.

At the other end, Loomis recorded the steepest decline, with its median sale price falling 16.8% from $817,000 to $679,649. Loomis is a small market — just 23 closings in the period — so the figure is sensitive to which homes traded. Orangevale fell 4.7% to $549,716, El Dorado Hills dropped 3.5% to $867,052, and Roseville slipped 2.8% to $629,175. Lincoln was nearly unchanged at $619,680, down 0.1% from $620,000 a year earlier.

Orangevale remains the most affordable city in the comparison on a median-price basis, followed by Lincoln and Roseville, all under $630,000. Granite Bay sits at the top, with El Dorado Hills and Folsom rounding out the high end above $750,000.

Sales activity: buyers return to most markets

Six of the eight cities saw more closings than a year ago, according to Redfin. Loomis led on a percentage basis, with sales up 35.3% (from 17 to 23), though again the small base makes the figure volatile. Folsom posted the most meaningful gain among larger markets, with closings up 22.1% to 221. El Dorado Hills sales rose 14.1% to 194, Orangevale climbed 13.2% to 86, Rocklin gained 4.3% to 168, and Roseville edged up 1.7% to 471 — the highest absolute sales count in the region.

Two cities saw sales decline. Lincoln slipped 1.9% to 258 closings, and Granite Bay fell 9.5% to 57. Granite Bay is the only market in the comparison where both falling sales and a longer time-on-market accompanied a sharp price increase, a combination that points to compositional shifts rather than uniform demand strength.

Speed and competition: Orangevale leads, Granite Bay lags

Orangevale was the fastest-moving market in the comparison, with a median of 12 days on market — two days slower than the year-ago figure of 10, but still the quickest in the region. Folsom followed at 14 days (up from 13), and Rocklin at 16 days (up from 15). Lincoln was the only market where homes sold faster than a year ago, with the median days-on-market falling from 24 to 22.

Granite Bay was the slowest market at 36 days, up sharply from 20 a year earlier. Loomis also slowed considerably, to 34 days from 25. Roseville (21 days, up from 18) and El Dorado Hills (23 days, up from 22) saw more modest increases.

On competitive intensity, Orangevale stands out: 48.8% of homes sold above list price, the highest share in the comparison, and the median sale-to-list ratio came in at 100.1% — the only city above 100%. Loomis followed with 40.9% of sales above list, and Rocklin (34.1%), Folsom (33.8%), Roseville (32.4%) and Lincoln (31.4%) clustered in the low-30s range. Granite Bay (26.8%) and El Dorado Hills (24.2%) had the smallest shares of above-list sales, consistent with their higher price points and slower sale times.

Inventory: supply tilts toward larger markets

Roseville carried the largest active inventory at 857 listings, followed by Lincoln (546), El Dorado Hills (443) and Folsom (409). Loomis had the thinnest active inventory in the comparison at 44 listings, with Granite Bay (139) and Orangevale (161) also relatively constrained.

On a sales-to-inventory basis, Orangevale and Folsom appear tightest: Orangevale’s 86 closings against 161 active listings, and Folsom’s 221 closings against 409, both pencil out to roughly a one-to-two ratio. Granite Bay’s 57 closings against 139 active listings — combined with its 36-day median time on market — points to a slower-moving high-end segment. New listings followed broadly similar patterns, with Roseville (603), Lincoln (381), Folsom (311) and El Dorado Hills (311) generating the most fresh supply.

Rents: a much narrower spread than home prices

Rental data from Zillow shows a far more compressed range across the region than sale prices. The highest median rent in the comparison is Granite Bay at $3,459 per month, followed by El Dorado Hills at $3,002. The lowest is Lincoln at $1,338 per month — less than 40% of Granite Bay’s figure, even though Lincoln’s median sale price ($619,680) is more than 40% of Granite Bay’s ($1,459,246). Orangevale ($2,088), Rocklin ($2,409), Roseville ($2,577) and Folsom ($2,611) fill the middle of the range.

Year-over-year rent changes were modest where comparison data is available. El Dorado Hills saw the largest increase, with rents up 3.4% from $2,903 to $3,002. Folsom rose 2.6% (from $2,545 to $2,611), Roseville gained 2.4% (from $2,516 to $2,577), and Lincoln climbed 1.9% (from $1,313 to $1,338). Rocklin and Orangevale were essentially flat, each up 0.3%. Zillow does not show a comparable year-ago figure for Granite Bay in this dataset, so no direction is stated there.

The rent-versus-buy picture differs sharply by city. Lincoln has the largest gap between rental costs and home prices in the comparison — its $1,338 median rent is the lowest in the region, while its $619,680 median sale price sits in the middle of the pack. Granite Bay and El Dorado Hills, by contrast, have the highest rents alongside the highest sale prices, suggesting their rental and ownership markets move more in tandem. Folsom and Rocklin show similar rents (within about $200 per month) despite Folsom’s median sale price being roughly $61,000 higher, while Orangevale offers the lowest median sale price in the comparison paired with a mid-range rent.

Reading the regional split

Taken together, the April data describes a Sacramento-area market where buyer activity is broadening — six of eight cities sold more homes than a year ago — but pricing power is concentrated. Outside of Granite Bay and Rocklin, year-over-year price gains have not materialized, and several mid-tier markets are running slightly below year-ago medians. Competitive metrics tell a similar story: the most heated bidding is occurring in lower-priced Orangevale and Loomis, where well over 40% of homes sold above list, while the most expensive markets (Granite Bay, El Dorado Hills) had the smallest above-list shares and the longest days on market.

National context frames the local picture. The 30-year fixed mortgage rate averaged 6.33% in April 2026, per Freddie Mac, about 39 basis points below the year-ago average of 6.72%, while the S&P/Case-Shiller national index was essentially unchanged year over year. Against that backdrop, Granite Bay’s 20.9% price gain reads as a local high-end anomaly — driven by a small number of transactions on slower-moving inventory — rather than a regional trend. The broader Sacramento-area pattern is one of returning sales activity paired with mostly flat-to-softer prices.